Delinquency in Argentina once again raised red flags. According to a report by the consulting firm 1816, prepared based on data from the Central Bank’s Debtors Center (CENDEU), in February there was a new increase in the level of credit default, with a particularly worrying figure: the strong deterioration in virtual wallets and non-banking entities.

“The credit irregularity of financial entities increased again in the month of February“says the report, which measures default as delays greater than 90 days.

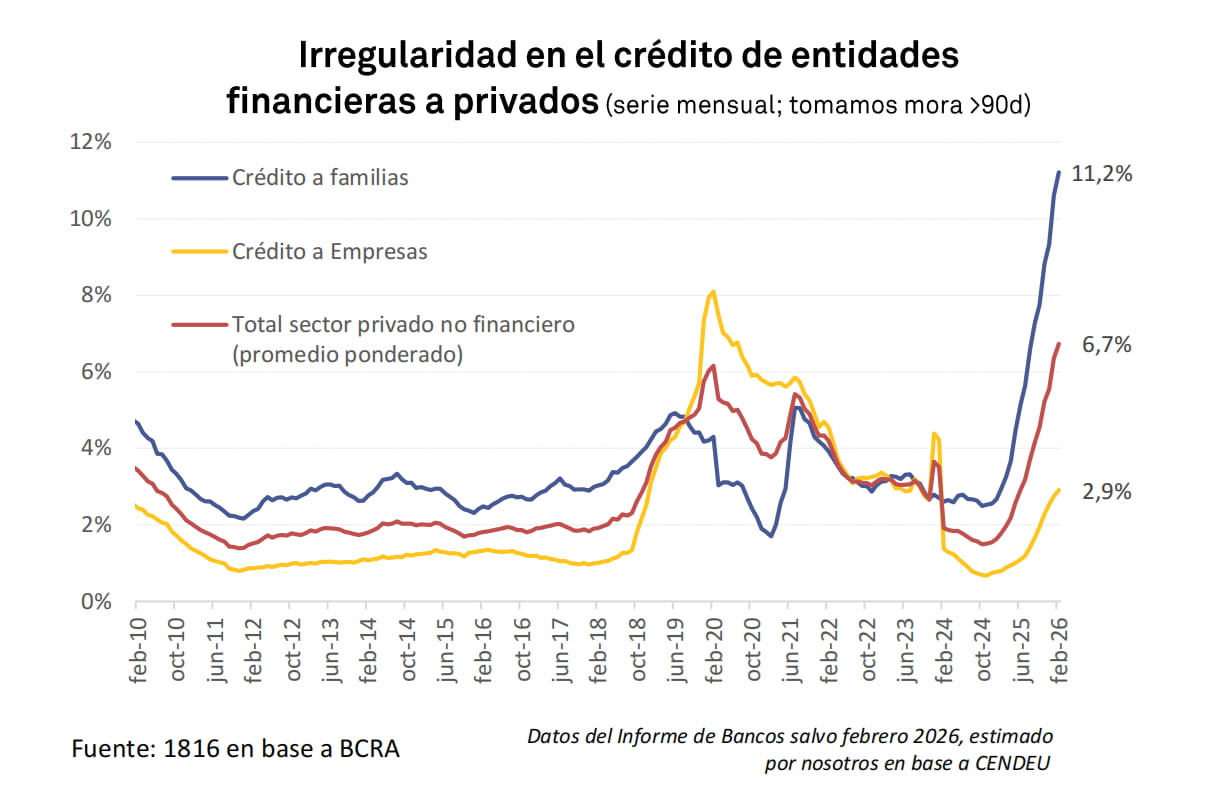

In general terms, The report shows that total delinquencies in the private sector went from 6.4% to 6.7% in just one month. But the focus is on homes, where the deterioration is most marked.

Families in red: record levels of delinquency

The family credit segment worsened again and has now accumulated more than a year of sustained deterioration. According to the report, Defaults in this segment rose from 10.6% in January to 11.2% in February.

The delinquency of families and companies with financial institutions deepened in February.

But the most relevant data is the underlying trend: “Family arrears rose for the sixteenth consecutive month and reached its highest value since 2004“warns the consultant.

This phenomenon occurs in a contradictory economic context: while some macro indicators show growth, large sectors of the population face difficulties in sustaining their financial commitments.

“The diagnosis at this point seems quite clear: the economy grows very heterogeneously“says the report, which highlights the contrast between dynamic sectors such as energy or mining and other more employment-intensive ones, such as commerce, industry and construction, which remain weakened.

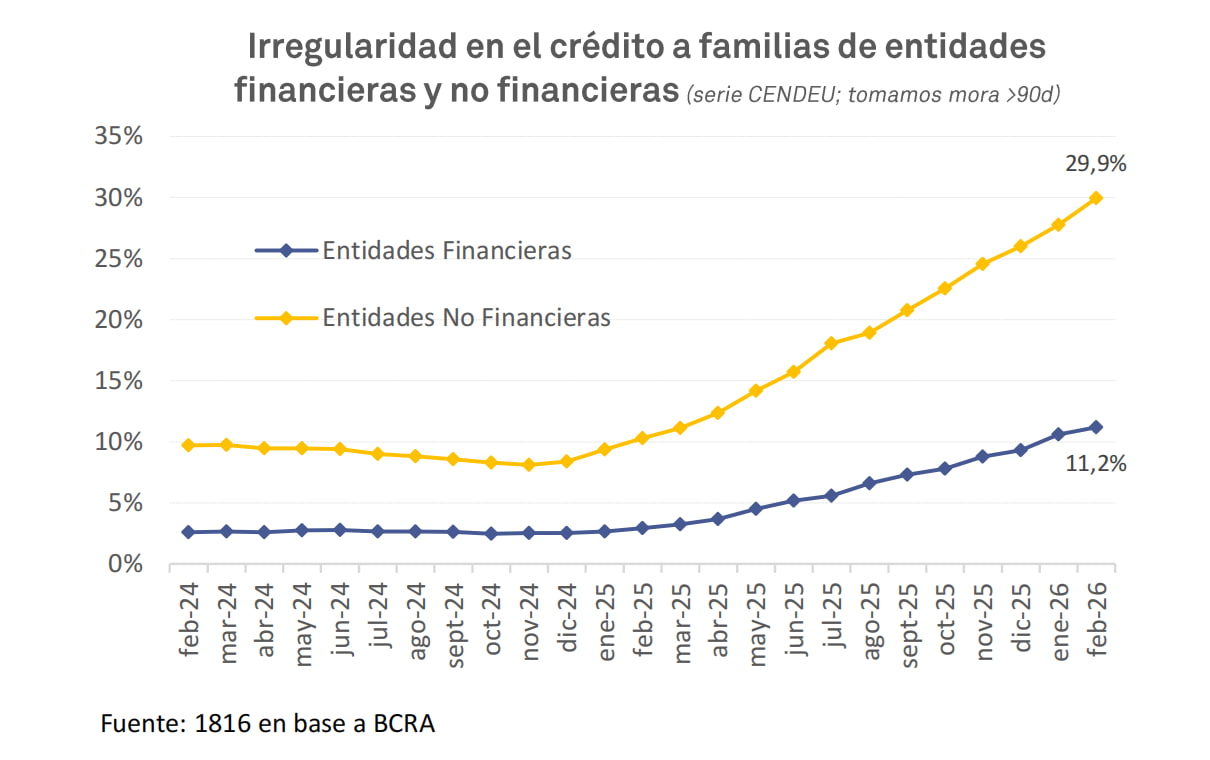

The default is almost 30% in virtual wallets and non-bank loans

The most critical point of the report appears when analyzing the behavior of non-financial entities, which include fintech, virtual wallets and credit grantors outside the traditional banking system.

There, the situation is noticeably more delicate: “Defaults on loans to households from non-financial entities also rose again, reaching 29.9% in February“, highlights the document.

The jump is significant: it implies an increase of more than two percentage points in just one month and leaves this segment with default levels almost three times higher than those of the banking system.

Although these entities represent close to 17% of total credit to families, their weight has been growing in recent years, which amplifies the impact of the deterioration.

Irregularities in loans from financial and non-financial entities to families skyrocketed.

A widespread phenomenon, not isolated cases

Another key point of the report is that the increase in arrears does not respond to specific problems of some entities, but rather to a widespread trend throughout the system.

“It is indisputable that irregularity continues to be a macro phenomenon and not something that can be explained by the credit policies of some banks.“, emphasizes the consultant.

In fact, The deterioration was verified in 28 of the 30 main financial entities in the countrywhich confirms the systemic nature of the problem.

High rates and pressure on income

The report also links the increase in delinquencies with the level of interest rates, which remain high despite some stability in the Central Bank’s reference rate.

Currently, personal loans present very demanding levels for household income: “Personal loan rates (…) are around 70%, which is equivalent to a TEA close to 100%“, details the report.

In the case of non-financial entities, the cost of credit is usually even higher, since it includes additional commissions and charges that increase the total financial cost.

Added to this is a context of deterioration in real income and increased unemployment during 2025, which limits the payment capacity of households.

Mercado Pago, hit by record late payments

The Delinquency in Argentina escalated to alarming levels during 2025. Mercado Pago tripled its irregularity ratio in just 12 months, according to official data from the Central Bank’s Debtors Center (CENDEU).

The largest virtual wallet in the country went from registering a default of 5.5% in January 2025 to reach 14.7% in January 2026. A jump that set off alarms in the financial sector.

The fintech of Marcos Galperin You are not alone in this crisis. The deterioration of payment capacity hit the entire system hard. The latest Report on Banks from the BCRA revealed that arrears on loans to households went from 2.67% to 10.6% in one year, the highest level in almost two decades.

The numbers reflect a vicious circle. Argentines ask for loans because their income is not enough to cover basic expenses. But later, They cannot pay those fees either.

Where is Mercado Pago located on the financial map

Non-banking entities face the worst situation. The delinquency in that segment approached 25% in early 2026.

Payment Market He remained in an intermediate step. With 14.7% irregularitywas located closer to traditional private banks than to non-banking financial companies, although without getting rid of the generalized problem of the system.

Company spokespersons consulted by Infobae maintained that the ratio is “in line with that of the main private banks” when looking at the segment of individuals. But there are important nuances.

The majority of Mercado Pago’s portfolio is aimed at individual consumers and families. That is, the segment hardest hit by the crisis. That is the public that suffers the most the deterioration of purchasing power.

A private survey with data as of December 2025 allows us to measure the differences. Orange Card record the highest default in the sector: 35.7%. A level that doubles that of Mercado Pago.

Mercado Libre, the unicorn that owns Mercado Pago, closed 2025 with 17.5% irregularity. Cencosud reached 25.5% and Consumption Credits reached 25.4%.

The Ualá case surprised the City and the company’s explanation

A few weeks ago, a post that went viral on social media generated alerts in the City: according to a user’s analysis, based on BCRA figures, Delinquency in Ualá reaches 40% of its portfolio. A fact that was later clarified by the digital wallet directed by Pierpaolo Barbieri.

The publication, made by the analyst Igor Ayusomentioned the alleged significant deterioration in the repayment of credits granted by fintech, in which it is observed how the difficulties of households to pay their financial obligations grow

The publication alluded to an alleged significant deterioration in the repayment of credits granted by fintech in a context in which the difficulties of households in meeting their financial obligations are growing.

But where the impact is strongest is in the fintech ecosystem. The Ualá case currently concentrates the market’s attention. Not only because of the level of arrears, but because of its composition.

The post by user Igor Ayuso, who based his report on data from the BCRA, In the banking segment of Ualá, defaults are around 43%. But in the non-financial business the number climbs to 63%. That data set off alarms in networks and part of the market.

What they said from Ualá

From Ualá they relativized the magnitude of the data. They noted that the firm discontinued credit origination under the peer-to-peer scheme in the middle of last year and transferred its best quality portfolio to its bank, which currently channels the loans.

From the company they maintain that, When purifying the information reported to the regulator, it would be around 18% in January and 17% in February.

“This implies that in this residual portfolio of the PSP there are mainly clients in default, without the entry of new credits to compensate for payers in situation. This significantly distorts the indicator,” unicorn sources warned.

Specifically, the firm that leads Pierpaolo Barbieri He said you shouldn’t mix pears with apples. “The values presented to the BCRA from financial entities usually apply the write-off practice, through which, after a certain period of uncollectibility, they eliminate unpaid credits from their balance sheets.”.

“Ualá will only begin to implement this mechanism in 2026so those cases continue to be reflected in their portfolio.” That is, the bad debts (which after a certain time come out of the bank figures) still persist in companies like the unicorn.

“If the same criteria used by the rest of the system were applied, allowing a homogeneous comparison, The default indicator as of February of the Ualá 2026 bank would be around 17%, an intermediate level with respect to the values observed in retail banking and fintechs,” they clarified.

Likewise, from Ualá they recognized the complex moment: “From mid-2025, The industry as a whole experienced a deterioration in the quality of the credit portfolio. “This led to a general tightening of credit policies and lower origination.”

“As a result, a double effect is produced: on the one hand, as credits in better situation are cancelled, the relative weight of delinquent cases within the stock increases; on the other, the context of high rates reduces the demand for credit by lower risk profiles,” they conclude.