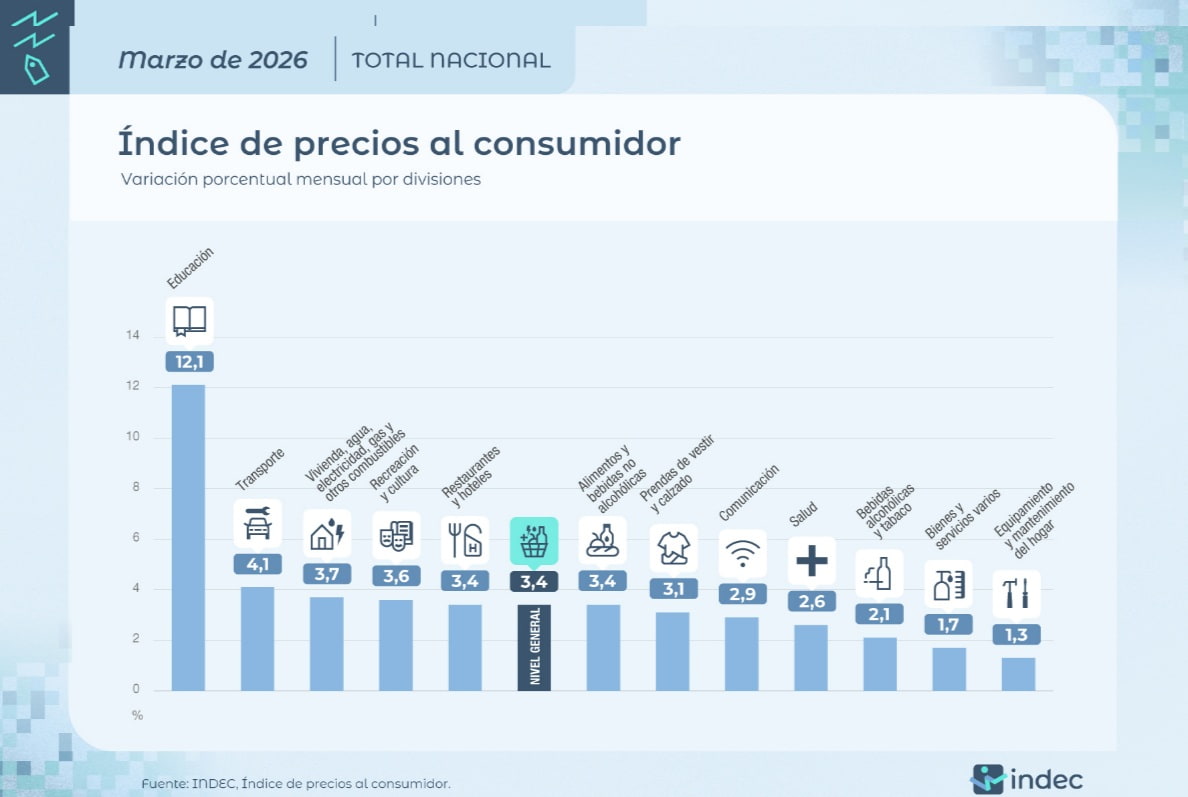

March inflation was at 3.4% and, as the market and even himself had anticipated, Luis Caputoaccelerated again after two consecutive months at 2.9%. This way, recorded the highest increase in a year: the figure for March 2025 had been 3.7%.

In this way, the inflation toaccumulated in the first three months of 2026 reached the 9.4%while year-on-year inflation was 32.6%.

In this way, inflation continued with a clearly upward trend. The CPI began to climb from May 2025when it registered an increase of 1.5%. After the 1.6% in June, had a variation of 1.9% in July and August, while it was 2.1% in September, 2.3% in October, 2.5% in November, 2.8% in December and finally 2.9% in January and February.

Inflation in March 2026 was the highest in a year

On Monday, during a presentation, Economy Minister Luis Caputo had anticipated that March inflation would rise again. Although he anticipated that it would tend to go down later: “It will surely be above 3% because there was a shock that evidently had an obvious impact on everything related to oil.from domestic plane tickets to transportation; You have topics like education, which in March has its seasonality. Starting in April, a process of disinflation and growth is coming, the best months are coming“, held.

The items that pushed the rise in inflation in March

The items that drove March inflation up

According to INDEC, at the category level, the Regulated prices (5.1%) had the largest increase due to adjustments in public service, transportation and education ratesfollowed by the core CPI (3.2%) – with a variation slightly lower than the general level – and Seasonal (1.0%), with increases linked to tourism and the change of season in clothing that compensated for the falls in prices of vegetables and fruits.

The division of greatest increase in the month was Education (12.1%): like every year, this increase coincides with the start of classes. The second division with the greatest increase was Transportation (4.1%) due to fuel, public transportation and air tickets.

The division with The greatest impact on the regional monthly variation was Food and non-alcoholic beveragesmainly due to the increase in Meat and derivatives (6.9% in GBA).

The two divisions that recorded the smallest variations in March 2026 were Miscellaneous goods and services (1.7%) and Home equipment and maintenance (1.3%).

Julian Neufeld, Economist from the Libertad y Progreso Foundation analyzed last month’s CPI: “The March data is overwhelming, 3.4% marks an inflation that has not fallen for 10 months. However, it is necessary to distinguish the incidence of phenomena external to monetary policy (of a transitory nature) from the component directly related to the dynamics between supply and demand of pesos. Within the first group we have as the main protagonist the effect of the war conflict in the Middle East, which had a full impact on national fuel prices, triggering the index towards the end of the month.”

“We can expect this impact to continue in the coming month, as the increase in oil prices spreads throughout the production chain. In view of the second group, for another month the regulated ones had a hard impact on inflation as a result of the policy of real appreciation of rates in CABA and greater Buenos Aires. In this way, the diagnosis remains the same: although current events may delay the disinflation process, to the extent that the BCRA maintains a restrictive monetary policy, we should observe an improvement towards the second half of this year,” he added.

April inflation: the first surveys and what the City anticipates

Lucio Garay Mendez, chief economist of EcoGo, does not rule out that the reduction in global energy supply, due to the paralysis in maritime traffic in the Strait of Hormuz due to the war in the Middle East, could extend for several more weeks and keep the international price of oil high, which would continue to put upward pressure on fuel prices. Therefore, estimates that the general level of the CPI for April and May, although it would decelerate, would probably would be above 2% monthly.

Camilo Tiscornia, director of C&T, estimates that the CPI for April “will give much less than in March, unless something crazy happens with gasoline.” Caprarulo agrees with this, and also estimates an inflationary slowdown in April, although “the big question remains the price of oil.” For the period between April and June, the director of Analytica projects a inflation around 2.6% monthly average.

“For April, we project a deceleration of inflation to 2.4% monthlyafter the 3% estimated for March. Inflation will remain high for the drag left by March (+10%)but it would weaken due to the drop in meat prices. In fact, if meat falls further, the slowdown could be even more pronounced. Furthermore, with the price of oil at US$101the gasoline continues with a 8% delay. If corrected during April, it could add 0.2 additional points of inflation,” adds the consulting firm. FMyA.

According to Max Capitalthe market expects the international price of oil to remain above last year’s levels, even if the conflict in the Middle East were to stop. Higher oil prices, he highlights, have implications for both inflation and external accounts, since it represents a “double edge shock” for an energy exporting country that seeks to reduce inflation and at the same time needs to accumulate reserves.

“The inflationary implications are similar to those of other countries, although the lack of a strong nominal anchor from the monetary side and greater inflationary inertia could generate a more pronounced impact. On the external side, however, part of the effect could be offset by a stronger currency thanks to higher mining and oil prices, along with a good agricultural harvest, Foreign Direct Investment (FDI) flows and debt issues also directed at these sectors,” he adds.

The broker maintains that the general effect of these dynamics would be:

- A slightly higher inflation

- A faster accumulation of international reserves

- A more appreciated currency in real terms

From a structural point of view, he highlights, “the shock reinforces recent dynamics, which favors energy and mining, sectors that are growing at a faster rate, but affects industrial production” due to the less competitiveness which implies a lower exchange rate in real terms.

Will inflation break 1% in August?: the market’s view

Although the consultants agree that once the rate adjustments and the seasonal peak in March have passed, inflation will return to the downward path, Javier Milei’s projection seems less and less feasible: The President reiterated on several occasions that In August of this year inflation could “start with zero”.

That is, in his words, it would register advances of less than 1% per month, such as 0.9% or less. Due to the latest variations and the inertia it exhibits, economists are cautious and consider it a very optimistic projection.

The spike in the international price of oil, due to the war in the Middle East and the fall in global crude oil supply, affects and could continue to affect inflationary dynamics. Until now, the impact has been felt partially in the internal costs of fuels and, indirectly, in the entire chain that arises from transportation, logistics and inputs. It is not the main reason for the acceleration in prices, but it provides a certain amount of upward pressure.

Meanwhile, at least for the moment, according to the BCRA’s Market Expectations Survey (REM), inflation will not pierce 1% in the short term.

The CPI trend will be downward in the coming months, according to the REM. The consultants estimate that it will be 2.6% in April, 2.3% in May, 2% in June and July and 1.8% in August and September. That is to say that, according to experts estimate, 2% will only be drilled in the eighth month of the year.

In all cases, Higher variations are expected than those anticipated in the previous REM: The impact of the war on prices can surely be one of the factors that experts take into account.

2026 would close with an inflation of 31.8%according to the consulting firms, which represents 3.1 pp more than the previous REM.